Measured yr/yr, real GDP increased by about 3.3% through Q2 '10.

Given that this 12 month period represents a full year of recovery,

this is a disappointing result. Partly, it reflects slower than expected

rebuilding of inventories in the wake of enormous inventory

liquidation during the recession. My coincident indicators -- real

wage change, total civilian employment, real retail sales and

industrial production -- were up 3.1% on a combined basis. One

factor that jumps out in looking at these indicators is how deeply

employment fell and also how the change in employment remains

negative still on a yr/yr basis. Safety net and stimulus programs

notwithstanding, the weak recovery of employment to date does

represent a serious loss of purchasing power in the economy.

The coincident indicators do not account for consumer savings

preference or for credit use. Consumers are rebuilding savings and

so far, credit use has been declining in the aggregate. So, collectively,

consumption has been on a cash and carry basis with occasional

dollops of funds squirreled into savings.

Real GDP when measured yr/yr should really be up between 5-6%

in the early stage of recovery and the shortfalls in consumer spending

and inventory re-investment are important factors behind the

lag in expected performance.

Long term, I peg real GDP growth potential for the US at 2.8% per

year. That is below the historic rate and reflects reduced

assumptions concerning labor force growth and labor participation

rates. It is far too early to reduce growth potential further, but it

is fair to acknowledge that the fist full year of recovery was a

disappointment. I can understand the fear and caution this

recession has created, particularly since it hit the work force,

household wealth, and the banking system so hard. For now, I am

trusting that continued recovery, however moderate, will allow

all major sectors to loosen up and behave with more confidence.

---------------------------------------------------------------

* I have many reservations about using GDP data, not the least

of which are the political ends it is used to serve. So I'll probably

only touch on it once a year or so.

Friday, July 30, 2010

Wednesday, July 28, 2010

Earnings & The Stock Market

The current cyclical recovery in corp. profits has been very powerful

so far. In history, it has only been matched by the massive jumps in

profits that occurred in the post WW1 economic recovery, the

surge off the Great Depression bottom in 1932, the immediate

post WW2 recovery and the great bounce after the 1937 recession.

The current surge in profits has exceeded most observers' initial

estimates by a country mile.

Grand surges in profits off depressed levels as recoveries begin can

last up to four years and fool more conservative expectations. It is

absolutely true that the exceptional earnings recovery over the past

year has been in part fueled by cost cutting, but yr/yr sales are up

about 9.5% by my count. The sales have provided the leverage

needed to produce the profit gains, and it is critical to note that

most companies have achieved recovering sales with just nominal

purchasing power. Plus, we can throw on about $200 bil. of loan

loss reserves that pared the total figure.

Let me stir the pot a little bit more. The bookend recessions of the

past decade have led to a large output gap between sales as booked

and sales that would have been booked under more normal trend

progress conditions. For SP 500 profits that "gap" is about $30 per

share or 42% of 12 months profits through July. History shows that

when a large output gap opens up in the wake of very poor economic

performance, only a portion of it is made back with the rest lost to

history. Even so, there is latent profits recovery of consequence in

store.

Most agree there is a slowdown of output growth ahead, and as I

discussed yesterday there is uncertainty over the likely progress of

liquidity growth needed to sustain economic recovery. When you

contrast this line of thought with the fact that profits have been

exploding upward, I think you will find a situation where without a

very sharp and extended slowdown in output growth, profits could

continue to run strong even if there is only a modest acceleration

in the growth of pricing power as economic recovery progresses.

And, you can see this tension playing out in the financial media.

Earnings are popping, but macro data suggests a slowdown ahead.

Now, even if profits growth goes ahead and moderates sharply, we

may well wind up with 12 month earning power for the Sp 500 at

decently high levels -- say $80 to 85 a share -- with much more

to come when the slowdown ends and the economy steps up some

in growth.

I guess if you pool today's post with yesterday's, what may shake out

is risk / uncertainty in the short run for stocks vs. the potential for

a big pay day if the economy regains moderate balance.

Ah, well, something to think about.

so far. In history, it has only been matched by the massive jumps in

profits that occurred in the post WW1 economic recovery, the

surge off the Great Depression bottom in 1932, the immediate

post WW2 recovery and the great bounce after the 1937 recession.

The current surge in profits has exceeded most observers' initial

estimates by a country mile.

Grand surges in profits off depressed levels as recoveries begin can

last up to four years and fool more conservative expectations. It is

absolutely true that the exceptional earnings recovery over the past

year has been in part fueled by cost cutting, but yr/yr sales are up

about 9.5% by my count. The sales have provided the leverage

needed to produce the profit gains, and it is critical to note that

most companies have achieved recovering sales with just nominal

purchasing power. Plus, we can throw on about $200 bil. of loan

loss reserves that pared the total figure.

Let me stir the pot a little bit more. The bookend recessions of the

past decade have led to a large output gap between sales as booked

and sales that would have been booked under more normal trend

progress conditions. For SP 500 profits that "gap" is about $30 per

share or 42% of 12 months profits through July. History shows that

when a large output gap opens up in the wake of very poor economic

performance, only a portion of it is made back with the rest lost to

history. Even so, there is latent profits recovery of consequence in

store.

Most agree there is a slowdown of output growth ahead, and as I

discussed yesterday there is uncertainty over the likely progress of

liquidity growth needed to sustain economic recovery. When you

contrast this line of thought with the fact that profits have been

exploding upward, I think you will find a situation where without a

very sharp and extended slowdown in output growth, profits could

continue to run strong even if there is only a modest acceleration

in the growth of pricing power as economic recovery progresses.

And, you can see this tension playing out in the financial media.

Earnings are popping, but macro data suggests a slowdown ahead.

Now, even if profits growth goes ahead and moderates sharply, we

may well wind up with 12 month earning power for the Sp 500 at

decently high levels -- say $80 to 85 a share -- with much more

to come when the slowdown ends and the economy steps up some

in growth.

I guess if you pool today's post with yesterday's, what may shake out

is risk / uncertainty in the short run for stocks vs. the potential for

a big pay day if the economy regains moderate balance.

Ah, well, something to think about.

Tuesday, July 27, 2010

Stock Market -- Fundamentals

The Window Of Uncertainty

Core fundamentals remain positive but do not exhibit the strength

seen throughout 2009. This indicator has only two settings --

positive and negative. When the core is positive, monetary policy

is relaxed, confidence is high or improving and interest rates, both

short and long are in cyclical low zones. The signal goes negative

when the Fed actively tightens credit via raising short rates and

draining reserves and bond yields begin to rise on a cyclical basis.

Negative core fundamentals do not imply an end to a cyclical bull

market, as credit growth usually supports rising output and profits.

But a negative signal suggests investors should either raise some

cash and/or trade in the shorter run, as the "easy money" has been

made.

The window of uncertainty we are now encountering involves an

interval of unknown duration in which reliance of the economy

switches from monetary liquidity growth to private sector credit

to sustain recovery / expansion. Usually, this transition is seamless

and occurs early in the recovery cycle. It has not happened yet,

and the uncertainty is poignant because the Fed, having loaded the

system with monetary liquidity in 2009, has stopped adding on the

assumption private sector credit demand would grow and take up

the slack. The latter has yet to occur. The Fed is jawboning banks to

lend and Bernanke has promised to take steps to add liquidity in

the interim if the recovery falters. But, if this interim period is

mishandled, we could have a situation wherein the recovery fails

and a cyclical bear market develops even though core fundamentals

are "positive".

Such a failure would be unprecedented and, I suspect, it is still too

early to tell if a failure is other than a remote possibility. But, my

indicators show that a seamless transition from monetary to credit

driven growth has yet to occur, so the unpleasant possibility of a

serious screw-up needs to be flagged.

Investors are aware of this particular uncertainty issue. And, over

May and June, when my weekly cyclical pressure gauge took a

tumble, the market reacted in a strongly negative way. The

weekly pressure gauge has leveled off, and investors no doubt are

heartened by strong Q 2 '10 profits results and the Fed's pledge to

address the liquidity issue as needed (See the 6/15 post for more on

the pressure gauge).

Indications that economic and profits growth are going to be easing

along with the uncertainty inherent in present monetary / credit

policy have led the market to trade at a significant discount to fair

value despite the recent strong advance off the 07/02 low. My

Market Tracker has fair value for the SP 500 at 1215 based on

estimated 12 mos. net per share through July. The discount stands

at 8.2% now, and was even an even larger 15.8% in early July. The

Tracker is a cyclical measure. On my long term model, the market is

now well priced under 1155 for holding periods beyond three years.

If you are kind enough to be reading along still, I can tell you the US

has not seen a situation quite like this for a good 100 years, if not

longer. It could all be wrapped up tidily and positively in a month or

so, or it could drag on, in which case the best and time honored

indicators would fail to signal correctly what to do and would leave

us to fly by the seats of our pants. I remain positive but watchful.

Core fundamentals remain positive but do not exhibit the strength

seen throughout 2009. This indicator has only two settings --

positive and negative. When the core is positive, monetary policy

is relaxed, confidence is high or improving and interest rates, both

short and long are in cyclical low zones. The signal goes negative

when the Fed actively tightens credit via raising short rates and

draining reserves and bond yields begin to rise on a cyclical basis.

Negative core fundamentals do not imply an end to a cyclical bull

market, as credit growth usually supports rising output and profits.

But a negative signal suggests investors should either raise some

cash and/or trade in the shorter run, as the "easy money" has been

made.

The window of uncertainty we are now encountering involves an

interval of unknown duration in which reliance of the economy

switches from monetary liquidity growth to private sector credit

to sustain recovery / expansion. Usually, this transition is seamless

and occurs early in the recovery cycle. It has not happened yet,

and the uncertainty is poignant because the Fed, having loaded the

system with monetary liquidity in 2009, has stopped adding on the

assumption private sector credit demand would grow and take up

the slack. The latter has yet to occur. The Fed is jawboning banks to

lend and Bernanke has promised to take steps to add liquidity in

the interim if the recovery falters. But, if this interim period is

mishandled, we could have a situation wherein the recovery fails

and a cyclical bear market develops even though core fundamentals

are "positive".

Such a failure would be unprecedented and, I suspect, it is still too

early to tell if a failure is other than a remote possibility. But, my

indicators show that a seamless transition from monetary to credit

driven growth has yet to occur, so the unpleasant possibility of a

serious screw-up needs to be flagged.

Investors are aware of this particular uncertainty issue. And, over

May and June, when my weekly cyclical pressure gauge took a

tumble, the market reacted in a strongly negative way. The

weekly pressure gauge has leveled off, and investors no doubt are

heartened by strong Q 2 '10 profits results and the Fed's pledge to

address the liquidity issue as needed (See the 6/15 post for more on

the pressure gauge).

Indications that economic and profits growth are going to be easing

along with the uncertainty inherent in present monetary / credit

policy have led the market to trade at a significant discount to fair

value despite the recent strong advance off the 07/02 low. My

Market Tracker has fair value for the SP 500 at 1215 based on

estimated 12 mos. net per share through July. The discount stands

at 8.2% now, and was even an even larger 15.8% in early July. The

Tracker is a cyclical measure. On my long term model, the market is

now well priced under 1155 for holding periods beyond three years.

If you are kind enough to be reading along still, I can tell you the US

has not seen a situation quite like this for a good 100 years, if not

longer. It could all be wrapped up tidily and positively in a month or

so, or it could drag on, in which case the best and time honored

indicators would fail to signal correctly what to do and would leave

us to fly by the seats of our pants. I remain positive but watchful.

Friday, July 23, 2010

Long Treasury Bond

The first try at a sustainable cyclical run-up in yield started in Half 2

2009. It was aborted in recent months as cycle growth measures and

inflation pressures eased, thus postponing any move by the Fed to

tighten credit overtly via raising benchmark short rates. The recent

downdraft in the bond's yield conforms perfectly with my monthly

broad macro economic yield indicator(data through June). Now, the

weekly cyclical pressure gauges I follow have started to level out

after falling sharply over May and most of June. This suggests the

long Treasury yield may stabilize around 4.0% as players assess

whether the weekly data could be signaling that the economy is set

to show more stability (See chart which compares the $TYX with

GS's industrial metals index.)

The long guy's yield is well inside its 40 wk m/a. This indicates an

overbought condition. My long term technical and fundamental

indicators also suggest the bond is currently overbought. Trader

advisories are also moving into the "too bullish" camp.

Fed chair Bernanke says the economic outlook is "unusually

uncertain" right ahead, so it is doubtful the Fed is going to

get fired up to raise short rates soon. However, the bond market

can easily trade plus or minus 50 basis points as players read

the weekly economic tea leaves over July and August.

2009. It was aborted in recent months as cycle growth measures and

inflation pressures eased, thus postponing any move by the Fed to

tighten credit overtly via raising benchmark short rates. The recent

downdraft in the bond's yield conforms perfectly with my monthly

broad macro economic yield indicator(data through June). Now, the

weekly cyclical pressure gauges I follow have started to level out

after falling sharply over May and most of June. This suggests the

long Treasury yield may stabilize around 4.0% as players assess

whether the weekly data could be signaling that the economy is set

to show more stability (See chart which compares the $TYX with

GS's industrial metals index.)

The long guy's yield is well inside its 40 wk m/a. This indicates an

overbought condition. My long term technical and fundamental

indicators also suggest the bond is currently overbought. Trader

advisories are also moving into the "too bullish" camp.

Fed chair Bernanke says the economic outlook is "unusually

uncertain" right ahead, so it is doubtful the Fed is going to

get fired up to raise short rates soon. However, the bond market

can easily trade plus or minus 50 basis points as players read

the weekly economic tea leaves over July and August.

Thursday, July 22, 2010

Cyclicals -- Relative Strength Measure

Cyclicals have just barely matched the market this year, but

the relative strength line(RSL) for the group has been holding

support and does not yet indicate that investors are ready

to go along with the "double dip" economic scenario. For

that, I think we would need a sharp break down in the RSL

for the group. Chart

the relative strength line(RSL) for the group has been holding

support and does not yet indicate that investors are ready

to go along with the "double dip" economic scenario. For

that, I think we would need a sharp break down in the RSL

for the group. Chart

Economic Free Fall -- Some After Effects

First, A Little History

When the Great Depression kicked off in 1929, US industrial

output plunged, falling by nearly 53% until mid-1932. As 1932

commenced, the Fed finally began injecting liquidity heavily into

the system. By Half 2 1932, production started to rebound and

rose by 62% over the next 12 months. It was difficult to balance

supply and demand within the economy with such long range

volatility, and not surprisingly, production fell by 20% over Half 2

1933, before enough balance was restored to enable the economy

to begin to recover more smoothly.

Economic Free Fall: Mid 2008 - Early 2009

My best guess is that we had experienced a mini replay of the

Depression over the 2008-09 period. From its 06/08 peak of

350.0, my index of the $value of US production plunged 15.7% to

a cyclical low of 295.0 in 04/09, before it recovered 9.4% to 322.8

in 06/10. By, post WW2 standards, this action reflects phenomenal

volatility, and I suspect it has proven difficult for households,

businesses and banks to adjust to it. Thus, we see a recovery in

retail sales, along with the paydown/liquidation of consumer

debt and an effort to boost personal savings. We see businesses

re-tooling equipment but only very reluctantly hiring. And then,

there are the banks. They stuffed loans in your pockets in 2005-06,

but now they are reluctant to lend to top quality smaller credits.

Mentality Not On Fast Forward

The economy has moved ahead, but many folks have yet to catch

up with it. Economic free fall and an initial quick bounce happened

so fast that restoring and maintaining balance and perspective have

been difficult to accomplish.

Something Not So Nice Is Ahead

Since the end of April, the weekly leading economic indicator sets

I use have declined sharply. Both have stabilized a bit in July, but

the damage has been heavy enough to signal that an economic

slowdown of some meaningful proportion lies ahead. The ECRI

WLI*, now watched very closely by throngs, has experienced a

two month decline that is consistent with development of an

economic recession. This index went into free fall from mid-2008

until early 2009, and then experienced its fastest rebound ever.

In fact, it rose by more than it normally rises in the first two

years after a recession and the decline it has experienced since the

end of April brings it down to a level consistent with a 12-14 month

timeline of recovery from a substantial recession.

Most of the classical elements which presage a recession are not

in place. What we do have are confidence levels across the spectrum

that are so low, that if folks do "freeze up" -- do not spend, do not

lend and do not hire, we could be in the soup.

Now I follow a very simple maxim: The money gets spent in the

USA. The Fed has added prodigiously to the basic money supply.

"Pushing on a string" is not an American economic concept. I think

we move forward with recovery, but its resumption could await

restoration of more of a sense of balance among the players and a

boost to confidence, which incidentally, can turn on a dime.

Now, in the next couple of months, we need to see folks loosen up

a little and get with the program. Such does not mean return of

prodigality but a balanced response to a recovering environment.

...................................................................................................................

* ECRI website.

When the Great Depression kicked off in 1929, US industrial

output plunged, falling by nearly 53% until mid-1932. As 1932

commenced, the Fed finally began injecting liquidity heavily into

the system. By Half 2 1932, production started to rebound and

rose by 62% over the next 12 months. It was difficult to balance

supply and demand within the economy with such long range

volatility, and not surprisingly, production fell by 20% over Half 2

1933, before enough balance was restored to enable the economy

to begin to recover more smoothly.

Economic Free Fall: Mid 2008 - Early 2009

My best guess is that we had experienced a mini replay of the

Depression over the 2008-09 period. From its 06/08 peak of

350.0, my index of the $value of US production plunged 15.7% to

a cyclical low of 295.0 in 04/09, before it recovered 9.4% to 322.8

in 06/10. By, post WW2 standards, this action reflects phenomenal

volatility, and I suspect it has proven difficult for households,

businesses and banks to adjust to it. Thus, we see a recovery in

retail sales, along with the paydown/liquidation of consumer

debt and an effort to boost personal savings. We see businesses

re-tooling equipment but only very reluctantly hiring. And then,

there are the banks. They stuffed loans in your pockets in 2005-06,

but now they are reluctant to lend to top quality smaller credits.

Mentality Not On Fast Forward

The economy has moved ahead, but many folks have yet to catch

up with it. Economic free fall and an initial quick bounce happened

so fast that restoring and maintaining balance and perspective have

been difficult to accomplish.

Something Not So Nice Is Ahead

Since the end of April, the weekly leading economic indicator sets

I use have declined sharply. Both have stabilized a bit in July, but

the damage has been heavy enough to signal that an economic

slowdown of some meaningful proportion lies ahead. The ECRI

WLI*, now watched very closely by throngs, has experienced a

two month decline that is consistent with development of an

economic recession. This index went into free fall from mid-2008

until early 2009, and then experienced its fastest rebound ever.

In fact, it rose by more than it normally rises in the first two

years after a recession and the decline it has experienced since the

end of April brings it down to a level consistent with a 12-14 month

timeline of recovery from a substantial recession.

Most of the classical elements which presage a recession are not

in place. What we do have are confidence levels across the spectrum

that are so low, that if folks do "freeze up" -- do not spend, do not

lend and do not hire, we could be in the soup.

Now I follow a very simple maxim: The money gets spent in the

USA. The Fed has added prodigiously to the basic money supply.

"Pushing on a string" is not an American economic concept. I think

we move forward with recovery, but its resumption could await

restoration of more of a sense of balance among the players and a

boost to confidence, which incidentally, can turn on a dime.

Now, in the next couple of months, we need to see folks loosen up

a little and get with the program. Such does not mean return of

prodigality but a balanced response to a recovering environment.

...................................................................................................................

* ECRI website.

Monday, July 19, 2010

Gold -- Interesting Period Ahead

Back on 6/27, with gold at $1256 oz., I posted that the metal was

riskier in price on several measures, including the fact that my gold

macro-directional indicator had diverged negatively from the price of

gold. I mentioned $60 oz. of near term price risk. Well, we closed the

day at $1183. A considerable portion of the overbought has been

removed, but, as the linked -to chart below shows, we have two

month downtrends on RSI and MACD, and a wave theorist might

argue that gold has completed a five wave up move with a recent

top that was fatigued on a momentum basis.

The fun element here is that since gold began its latest uptrend in late

2008, the bugs have come in to buy all of the dips between 30 -40

on RSI. RSI on today's close is 40, so it will be interesting to see if

the bugs are set to launch a rescue effort and rally the stuff. A

significant break of trend, and gold is close to it, could be on the

nasty side if the gold buffs sit this one out.

Gold chart.

riskier in price on several measures, including the fact that my gold

macro-directional indicator had diverged negatively from the price of

gold. I mentioned $60 oz. of near term price risk. Well, we closed the

day at $1183. A considerable portion of the overbought has been

removed, but, as the linked -to chart below shows, we have two

month downtrends on RSI and MACD, and a wave theorist might

argue that gold has completed a five wave up move with a recent

top that was fatigued on a momentum basis.

The fun element here is that since gold began its latest uptrend in late

2008, the bugs have come in to buy all of the dips between 30 -40

on RSI. RSI on today's close is 40, so it will be interesting to see if

the bugs are set to launch a rescue effort and rally the stuff. A

significant break of trend, and gold is close to it, could be on the

nasty side if the gold buffs sit this one out.

Gold chart.

Friday, July 16, 2010

Inflation Situation

The CPI hit an all-time peak of 220.0 in 07/08. With recession in

full flower, it fell to an interim low of 210.2 in 12/08. The CPI has

recovered most of the decline since, but stands now at 218.0 for

June. Thus, technically, the US is still in deflation and more so

when you view asset deflation such as losses in home values and the

SP 500 over recent years.

From the interim low of 210.2 set 12/08, the CPI recovered by 3.7%

through 04/10, but has flattened out recently on weakness in the

commodities market and a continuing deceleration of the CPI

excluding food and fuels. The inflation pressure gauges I use did

peak over the Mar. / Apr. period and remain sluggish. My longer

term pressure gauge, which was signaling a sharp rise of inflation

in 2011, has moderated very substantially since the spring of 2010.

One key gauge of inflation potential, the capacity utilization rate,

stands at 74.1%, which is very low for the post WW2 period, and

is well below the the 80% level, when pricing pressures tend to pop.

Prospects for a moderation in the growth of China's manufacturing

output has put a chill on commodities prices, and is proving

beneficial to the US on the inflation front.

Measured yr/yr, the CPI was up by 1.1% through 06/10, and it

may well stay subdued until positive interest returns to the

commodities market. Commodities composites have bounced a bit in

recent weeks, but have yet to challenge a mild downtrend now in

place. CRB chart. When looking at inflation potential, you need to

watch commodities and oil in particular like a hawk.

The supply / demand equation for petroleum products and for

industrial commodities has tightened appreciably over the past

decade in comparison to the 1980s - 1990s. With Asia (ex. Japan)

and South America now sporting more vibrant economies, I have

developed a GDP weighted global total economic supply/ demand

pressure gauge. It has recovered substantially from its recession

low in early 2009, but at a current reading of 132.0 is well below

the 140 - 145 range that would suggest global inflation pressure

and an intense run-up in petroleum and industrial commodities

that could force sharp synchronous credit tightening by major

central banks. We are still in a "cool zone" now. One lesson from

the global gauge is that the US can experience cyclical inflation

pressure if the world is running hotter but the US is still running

well below effective capacity.

full flower, it fell to an interim low of 210.2 in 12/08. The CPI has

recovered most of the decline since, but stands now at 218.0 for

June. Thus, technically, the US is still in deflation and more so

when you view asset deflation such as losses in home values and the

SP 500 over recent years.

From the interim low of 210.2 set 12/08, the CPI recovered by 3.7%

through 04/10, but has flattened out recently on weakness in the

commodities market and a continuing deceleration of the CPI

excluding food and fuels. The inflation pressure gauges I use did

peak over the Mar. / Apr. period and remain sluggish. My longer

term pressure gauge, which was signaling a sharp rise of inflation

in 2011, has moderated very substantially since the spring of 2010.

One key gauge of inflation potential, the capacity utilization rate,

stands at 74.1%, which is very low for the post WW2 period, and

is well below the the 80% level, when pricing pressures tend to pop.

Prospects for a moderation in the growth of China's manufacturing

output has put a chill on commodities prices, and is proving

beneficial to the US on the inflation front.

Measured yr/yr, the CPI was up by 1.1% through 06/10, and it

may well stay subdued until positive interest returns to the

commodities market. Commodities composites have bounced a bit in

recent weeks, but have yet to challenge a mild downtrend now in

place. CRB chart. When looking at inflation potential, you need to

watch commodities and oil in particular like a hawk.

The supply / demand equation for petroleum products and for

industrial commodities has tightened appreciably over the past

decade in comparison to the 1980s - 1990s. With Asia (ex. Japan)

and South America now sporting more vibrant economies, I have

developed a GDP weighted global total economic supply/ demand

pressure gauge. It has recovered substantially from its recession

low in early 2009, but at a current reading of 132.0 is well below

the 140 - 145 range that would suggest global inflation pressure

and an intense run-up in petroleum and industrial commodities

that could force sharp synchronous credit tightening by major

central banks. We are still in a "cool zone" now. One lesson from

the global gauge is that the US can experience cyclical inflation

pressure if the world is running hotter but the US is still running

well below effective capacity.

Wednesday, July 14, 2010

Financial Liquidity & Banking System

Liquidity

There has been little change in my broad credit-driven measure of

financial liquidity in months. On balance, private sector credit

demand has remained lax, so banks have done little to create or

compete for the deposits that would touch off faster broad liquidity

growth. Interestingly, the Fed did ease along with monetary

liquidity in June, which it will need to continue to do if private sector

credit demand does not recover. The Fed is looking at its options in

this regard.

The Fed's outreach programs show that some bankers are reluctant

to lend to smaller businesses with strong cash flows because of

concern over collateral values and is indicating to banks that healthy

debt service capability should receive more priority. It is also clear

that even though FICO credit scores for households have slipped only

slightly over the past two years, banks are employing more stringent

standards in extending consumer credit. So, even though credit

demand has been modest in this economic recovery to date, it is

becoming more clear that bankers are also maintaining conservative

practices adopted in the immediate wake of the financial crisis. This is

a natural development given the grand magnitude of loan losses the

banks have piled up over the past two years, but at some point

before too long, they are going need to loosen up a little, especially

with regard to business credit.

Banking System

As is typical of recession / post recession periods, the banks have

been letting the total system loan / lease book run off. On a revised

basis the run off has been roughly $600 bil. or 6.2%. Even so, the

L&L book remains about $400 bil. over the long term trend as the

banks bring the book slowly into line with trend. By the same token,

banks have substantially increased their investment portfolios, and

my flash liquidity indicator (Treasuries vs. shorter term business

loans) has shown marked improvement. Bank capital has been

growing, and loan loss reserves have recently shown more stability.

It was also good to see that both consumer loans and commercial &

industrial loans showed stability in June, after lengthy declines. The

banks have a considerable way to go to get back into long term

balance, but there has been enough improvement to enable them to

participate in the economic recovery in a moderate way.

There has been little change in my broad credit-driven measure of

financial liquidity in months. On balance, private sector credit

demand has remained lax, so banks have done little to create or

compete for the deposits that would touch off faster broad liquidity

growth. Interestingly, the Fed did ease along with monetary

liquidity in June, which it will need to continue to do if private sector

credit demand does not recover. The Fed is looking at its options in

this regard.

The Fed's outreach programs show that some bankers are reluctant

to lend to smaller businesses with strong cash flows because of

concern over collateral values and is indicating to banks that healthy

debt service capability should receive more priority. It is also clear

that even though FICO credit scores for households have slipped only

slightly over the past two years, banks are employing more stringent

standards in extending consumer credit. So, even though credit

demand has been modest in this economic recovery to date, it is

becoming more clear that bankers are also maintaining conservative

practices adopted in the immediate wake of the financial crisis. This is

a natural development given the grand magnitude of loan losses the

banks have piled up over the past two years, but at some point

before too long, they are going need to loosen up a little, especially

with regard to business credit.

Banking System

As is typical of recession / post recession periods, the banks have

been letting the total system loan / lease book run off. On a revised

basis the run off has been roughly $600 bil. or 6.2%. Even so, the

L&L book remains about $400 bil. over the long term trend as the

banks bring the book slowly into line with trend. By the same token,

banks have substantially increased their investment portfolios, and

my flash liquidity indicator (Treasuries vs. shorter term business

loans) has shown marked improvement. Bank capital has been

growing, and loan loss reserves have recently shown more stability.

It was also good to see that both consumer loans and commercial &

industrial loans showed stability in June, after lengthy declines. The

banks have a considerable way to go to get back into long term

balance, but there has been enough improvement to enable them to

participate in the economic recovery in a moderate way.

Sunday, July 11, 2010

OEX 100 Put / Call Ratio

The OEX 100 (big caps) was an early entrant in the index option

derby and was probably one of the most popular for a number of

years. Normally, the OEX put / call ratio exceeds 1.00 as larger

players use puts to hedge long equity positions, either as a genaral

strategy or for OEX baskets held long. It is unusual to see the

put / call ratio below 1.00 because the players are then net long

and unhedged in total. Having traded OEX options for so many

years, I keep an eye on the P/C ratio if only for old time's sake.

The ratio went below 1.00 with some consistency toward the end

of 2008 and stayed low well into the early part of 2009. Partly,

this no doubt reflected the rising cost of options and the fact that

long OEX baskets had been sold out, but I also concluded the

bigger players believed the bear market was ending. We have a

similar situation today, and again, I have concluded that the bulk

of the corrective action may have been taken.

I also watch the OEX P/C ratio against the CBOE individual

equities P/C ratio. I have noticed that there are cases when the

OEX P/C is a whopping 1.5 and the CBOE is just .50. More

often than not, the OEX put buyers have been right and the

market is toppy. So too when the OEX is below 1.00 and the

CBOE is slightly elevated, say above .60. The market at these

times is more likely to be sold out.

This type of comparison does not work all the time, and it

requires a bit of a guess as to when to pay attention to it. But,

I have to say I am usually comfortable with comparisons of

this sort.

OEX put / call ratio chart. (Two looks).

derby and was probably one of the most popular for a number of

years. Normally, the OEX put / call ratio exceeds 1.00 as larger

players use puts to hedge long equity positions, either as a genaral

strategy or for OEX baskets held long. It is unusual to see the

put / call ratio below 1.00 because the players are then net long

and unhedged in total. Having traded OEX options for so many

years, I keep an eye on the P/C ratio if only for old time's sake.

The ratio went below 1.00 with some consistency toward the end

of 2008 and stayed low well into the early part of 2009. Partly,

this no doubt reflected the rising cost of options and the fact that

long OEX baskets had been sold out, but I also concluded the

bigger players believed the bear market was ending. We have a

similar situation today, and again, I have concluded that the bulk

of the corrective action may have been taken.

I also watch the OEX P/C ratio against the CBOE individual

equities P/C ratio. I have noticed that there are cases when the

OEX P/C is a whopping 1.5 and the CBOE is just .50. More

often than not, the OEX put buyers have been right and the

market is toppy. So too when the OEX is below 1.00 and the

CBOE is slightly elevated, say above .60. The market at these

times is more likely to be sold out.

This type of comparison does not work all the time, and it

requires a bit of a guess as to when to pay attention to it. But,

I have to say I am usually comfortable with comparisons of

this sort.

OEX put / call ratio chart. (Two looks).

Saturday, July 10, 2010

Stock Market --Technical

The SP 500 popped up enough last week to set up a challenge of the

downtrend in force over the past two months. For trend followers,

there is promise but no confirmation of a positive reversal, either

short or intermediate term. In fact, 13-14 wk indicators are still

negative.

We have had three legs down on this correction, so the challenge

of the downtrend line ahead may be more forceful. I must say,

however, that I very much dislike seeing a week end with a challenge

in view only to see it be postponed. That will prompt some trend line

traders to have reservations.

My NYSE buying pressure index has not broken down, and the

selling pressure index has failed to sustain a rise. When I look at

advances vs. declines on a rolling six wk. basis, there is net

accumulation underway, but there is nothing smooth about it. As

the chart link below shows, the cumulative NYSE adv / dec line

has held support well, has broken through its downtrend line and

is just turning positive on MACD. I am also heartened by the

dramatic improvement in the TRIN last week following an

extended interval of capitulation.

In short, the market is getting close, but has yet to earn the cigar

in the near term.

NYSE A /D chart.

downtrend in force over the past two months. For trend followers,

there is promise but no confirmation of a positive reversal, either

short or intermediate term. In fact, 13-14 wk indicators are still

negative.

We have had three legs down on this correction, so the challenge

of the downtrend line ahead may be more forceful. I must say,

however, that I very much dislike seeing a week end with a challenge

in view only to see it be postponed. That will prompt some trend line

traders to have reservations.

My NYSE buying pressure index has not broken down, and the

selling pressure index has failed to sustain a rise. When I look at

advances vs. declines on a rolling six wk. basis, there is net

accumulation underway, but there is nothing smooth about it. As

the chart link below shows, the cumulative NYSE adv / dec line

has held support well, has broken through its downtrend line and

is just turning positive on MACD. I am also heartened by the

dramatic improvement in the TRIN last week following an

extended interval of capitulation.

In short, the market is getting close, but has yet to earn the cigar

in the near term.

NYSE A /D chart.

Friday, July 09, 2010

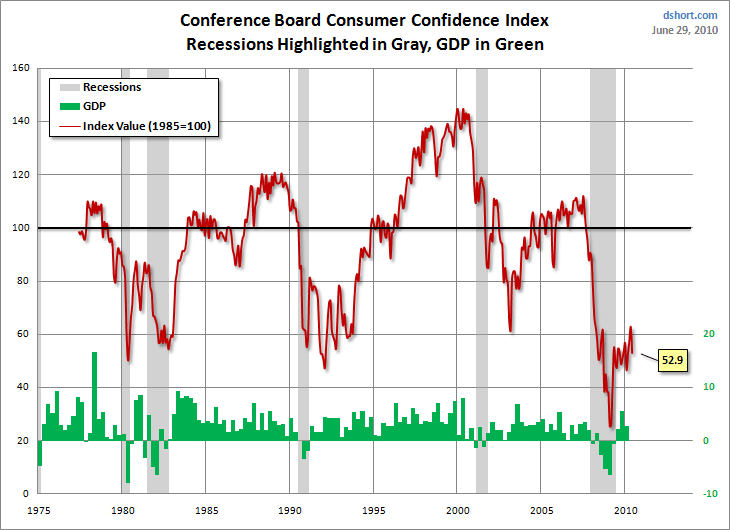

Consumer Credit

Consumer credit -- excluding mortgages -- declined again May, and

it is down about 7% from the peak of nearly $2.6 tril. in 2008. This

no doubt reflects the severe decline and only partial recovery of

retail sales over the period, but It is also probably an outcome to be

expected given the extraordinary plummet in consumer confidence

as well. Confidence has recovered modestly over the past year, but

it is just coming up to the lows registered after prior economic

declines. Chart.

The chart does show an extended period of low confidence in the

early 1990s. Back then, the housing market was also weak, and there

was a surge in so-called white collar layoffs not seen before in the

post WW 2 era over the same interval. Noteworthy is that total

consumer credit was flat over most of the 1990 - 93 period before

recovering.

I am reluctant to say we have entered a "new normal" era of

consumer deleveraging or credit use austerity, as it seems that the

round of revolving credit paydown / default we have witnessed in

this cycle reflects the depth of the recession and the pounding

consumer confidence has taken -- weaker home prices, damaged

retirement savings, a depressed job market. I think it is too early

in the game to posit a new era of austerity and that we need to

first see how confidence responds to continued economic recovery.

it is down about 7% from the peak of nearly $2.6 tril. in 2008. This

no doubt reflects the severe decline and only partial recovery of

retail sales over the period, but It is also probably an outcome to be

expected given the extraordinary plummet in consumer confidence

as well. Confidence has recovered modestly over the past year, but

it is just coming up to the lows registered after prior economic

declines. Chart.

{kind=link}

The chart does show an extended period of low confidence in the

early 1990s. Back then, the housing market was also weak, and there

was a surge in so-called white collar layoffs not seen before in the

post WW 2 era over the same interval. Noteworthy is that total

consumer credit was flat over most of the 1990 - 93 period before

recovering.

I am reluctant to say we have entered a "new normal" era of

consumer deleveraging or credit use austerity, as it seems that the

round of revolving credit paydown / default we have witnessed in

this cycle reflects the depth of the recession and the pounding

consumer confidence has taken -- weaker home prices, damaged

retirement savings, a depressed job market. I think it is too early

in the game to posit a new era of austerity and that we need to

first see how confidence responds to continued economic recovery.

Wednesday, July 07, 2010

Stock Market Psychology

The market has been doggedly following short term economic

factors, particularly the ECRI leading index, weekly unemployment

claims, sensitive materials prices and the 2 yr. Treas. note yield.

At first, I thought strength so far this week might reflect other

positive economic signs such as a large increase in global chip sales

and indications retail store sales were pretty decent in June. Then,

I checked in with "Dr. Copper", one of the better economic

forecasters around, only to find that the copper price has started to

edge up in recent days. Since copper is one of the more important

of the group of industrial commodities, action in this market may

be receiving unusually heavy scrutiny by stock traders. This would

also suggest that the market might still be retaining its narrow

short term focus on near-in fundamentals. Copper.

factors, particularly the ECRI leading index, weekly unemployment

claims, sensitive materials prices and the 2 yr. Treas. note yield.

At first, I thought strength so far this week might reflect other

positive economic signs such as a large increase in global chip sales

and indications retail store sales were pretty decent in June. Then,

I checked in with "Dr. Copper", one of the better economic

forecasters around, only to find that the copper price has started to

edge up in recent days. Since copper is one of the more important

of the group of industrial commodities, action in this market may

be receiving unusually heavy scrutiny by stock traders. This would

also suggest that the market might still be retaining its narrow

short term focus on near-in fundamentals. Copper.

Monday, July 05, 2010

Stock Market -- Technical

1) The market is moderately oversold on a price momentum basis

for the short term, and it is closing in on exhaustion of the sell-off.

NYSE breadth has held up better than has price momentum, and

the market is not oversold but is neutral on these measures. My

breadth indicators, when oversold, are more reliable than the

price momentum measures. The SP 500 closed out last week at

1023. Next support level is 1000.

2) My biggest technical concern during the nearly 13 month long

80% leg-up in the market off the 03/09 low was that the angle of

the trajectory was simply too steep and that at some point investors

would be faced with an extended consolidation / sell-off interval

before there could be another durable up-move. Much, but not all

of that risk, has been removed over the past couple of months.

3) For many years, I have used a price oscillator determined weekly

off the 40 wk m/a. Toward the end of 2009, that oscillator (the

premium / discount in price off the 40 wk m/a) reached extended

levels not seen since the bubble years of 1997 - 99. Now, the market

has swung to a discount steep enough to be consistent with a

developing bear market. The current reading is neutral between

whether a cyclical bear is in force or whether we face a steep price

correction in an ongoing cyclical bull (a kind of "economic slowdown

shock"). Since the volatility in the market (and in the economy) has

been so great over the past two years, I think it is simply premature

to call a cyclical bear, and I am remaining in the bull camp for now.

Strategy

As discussed last week, I am presently long the market. But, I

envision running a personal hedge fund primarily using options

to hedge my position in various ways until we see a diminution in

economic volatility which I freely concede might not occur until

another 12 months has gone bye the bye. (I have traded call and

put options since the mid-1970s. Such trading can be a vexing

and frustrating affair, particularly as regards order execution. I

enjoy it overall, but such trading is not for everyone. Practice first

for an extended period before you try for real.)

I have linked to a weekly chart for the SP 500 which suggests the

market may also be close to an exhaustion of the recent sell-off.

Chart.

for the short term, and it is closing in on exhaustion of the sell-off.

NYSE breadth has held up better than has price momentum, and

the market is not oversold but is neutral on these measures. My

breadth indicators, when oversold, are more reliable than the

price momentum measures. The SP 500 closed out last week at

1023. Next support level is 1000.

2) My biggest technical concern during the nearly 13 month long

80% leg-up in the market off the 03/09 low was that the angle of

the trajectory was simply too steep and that at some point investors

would be faced with an extended consolidation / sell-off interval

before there could be another durable up-move. Much, but not all

of that risk, has been removed over the past couple of months.

3) For many years, I have used a price oscillator determined weekly

off the 40 wk m/a. Toward the end of 2009, that oscillator (the

premium / discount in price off the 40 wk m/a) reached extended

levels not seen since the bubble years of 1997 - 99. Now, the market

has swung to a discount steep enough to be consistent with a

developing bear market. The current reading is neutral between

whether a cyclical bear is in force or whether we face a steep price

correction in an ongoing cyclical bull (a kind of "economic slowdown

shock"). Since the volatility in the market (and in the economy) has

been so great over the past two years, I think it is simply premature

to call a cyclical bear, and I am remaining in the bull camp for now.

Strategy

As discussed last week, I am presently long the market. But, I

envision running a personal hedge fund primarily using options

to hedge my position in various ways until we see a diminution in

economic volatility which I freely concede might not occur until

another 12 months has gone bye the bye. (I have traded call and

put options since the mid-1970s. Such trading can be a vexing

and frustrating affair, particularly as regards order execution. I

enjoy it overall, but such trading is not for everyone. Practice first

for an extended period before you try for real.)

I have linked to a weekly chart for the SP 500 which suggests the

market may also be close to an exhaustion of the recent sell-off.

Chart.

Friday, July 02, 2010

Economic & Profits Indicators

Weekly leading indicators have recently stabilized after a

sudden and wrenching downturn running through May and mid-

June. But there has been an unmistakable signal that slowing

of recovery progress lies ahead. Monthly leading indicators also

signal a slowdown, but have held up better than the weeklies. The

recovery surge in the monthly indicators from early 2009 was not

exceptional at all, while the lift off in the weeklies was the strongest

in the modern era. When the weeklies such as the ECRI set are

viewed in the context of the first 24 months of recovery, the recent

weakness brings them down to average from super-strong. the

weeklies in the US line up best with the powerful recovery of

export sales and factory orders and less so compared to the broader

economy.

My economic power index, which focuses on the real wage and

the change of total employment, has been slow to recover. The

real wage, measured yr/yr is flat. This reflects weak labor market

conditions, but it also continues a trend of business to not reward

labor for productivity improvement but to let rewards flow entirely

to capital instead. Investors applaud the practice on an individual

company level, but, when seen in the aggregate, it undermines the

purchasing power of the economy and leads to a reduction in the

efficiency of $ capital. The index results also show companies have

been slow to rehire, preferring to "milk" current operations as

fully as possible. The salutary here for workers is that real take

home pay is up 1.6% yr/yr entirely as a result of more hours

worked plus OT.

The slow recovery of the EPI coupled with wage earner attempts

to replenish savings and avoid dipping into credit has created an

environment that supports modest and not robust economic

progress.

Profits indicators were very strong through the first five

months of 2010, but they did moderate in June, and the leading

indicators now suggest further moderation as the year progresses.

My long term leading economic indicators were the

strongest ever at the end of 2008. The indicators have lost

strength since then but remain positive and continue to support

economic and profits recovery through 2011. However, I am

concerned that the Fed not be asleep at the switch and that It

will be prepared to provide additional monetary liquidity to the

system if private sector credit demand -- now basing -- does not

show decent lift by this year's end.

sudden and wrenching downturn running through May and mid-

June. But there has been an unmistakable signal that slowing

of recovery progress lies ahead. Monthly leading indicators also

signal a slowdown, but have held up better than the weeklies. The

recovery surge in the monthly indicators from early 2009 was not

exceptional at all, while the lift off in the weeklies was the strongest

in the modern era. When the weeklies such as the ECRI set are

viewed in the context of the first 24 months of recovery, the recent

weakness brings them down to average from super-strong. the

weeklies in the US line up best with the powerful recovery of

export sales and factory orders and less so compared to the broader

economy.

My economic power index, which focuses on the real wage and

the change of total employment, has been slow to recover. The

real wage, measured yr/yr is flat. This reflects weak labor market

conditions, but it also continues a trend of business to not reward

labor for productivity improvement but to let rewards flow entirely

to capital instead. Investors applaud the practice on an individual

company level, but, when seen in the aggregate, it undermines the

purchasing power of the economy and leads to a reduction in the

efficiency of $ capital. The index results also show companies have

been slow to rehire, preferring to "milk" current operations as

fully as possible. The salutary here for workers is that real take

home pay is up 1.6% yr/yr entirely as a result of more hours

worked plus OT.

The slow recovery of the EPI coupled with wage earner attempts

to replenish savings and avoid dipping into credit has created an

environment that supports modest and not robust economic

progress.

Profits indicators were very strong through the first five

months of 2010, but they did moderate in June, and the leading

indicators now suggest further moderation as the year progresses.

My long term leading economic indicators were the

strongest ever at the end of 2008. The indicators have lost

strength since then but remain positive and continue to support

economic and profits recovery through 2011. However, I am

concerned that the Fed not be asleep at the switch and that It

will be prepared to provide additional monetary liquidity to the

system if private sector credit demand -- now basing -- does not

show decent lift by this year's end.

Subscribe to:

Posts (Atom)